We’ve hit the midpoint of 2016, which makes it a great time to review your portfolio and shop for some top-notch dividend-growth stocks as we head into the back half of 2016.

In a moment, I’ll give you three of my favorites to buy now.

The good news? With the market up just 2.4% so far this year, buying now means you probably won’t pay much more than you would have back in January.

As I’m sure you’ll recall, the S&P 500’s nosedive started before we’d even put the New Year’s confetti away. By mid-February, it had shed 11% of its value.

As I’m sure you’ll recall, the S&P 500’s nosedive started before we’d even put the New Year’s confetti away. By mid-February, it had shed 11% of its value.

But if you’re a regular reader, you’ll also recall that we were ready to pounce when the market bottomed on February 11.

[ad#Google Adsense 336×280-IA]The day before, I gave you 3 unloved REITs to buy straightaway—and they’ve all demolished the index’s subsequent 12% rise: Ventas Inc. (VTR) exploded for a 44% gain, while HCP Inc. (HCP) soared 30%.

The Vanguard REIT Index Fund (VNQ), took off on a 21% run.

The S&P 500 had just struggled back into the black on the year when last week’s Brexit knocked it for a loop again, slicing 5.6% off its value (it’s since regained most of that ground).

Two days later, I gave you two closed-end funds to shield your portfolio from nasty surprises like Brexit in the future, as well as two bargain stock buys it left in its wake.

But what about the next six months?

One thing that’s certainly off the table is an interest rate hike. Brexit has put paid to that.

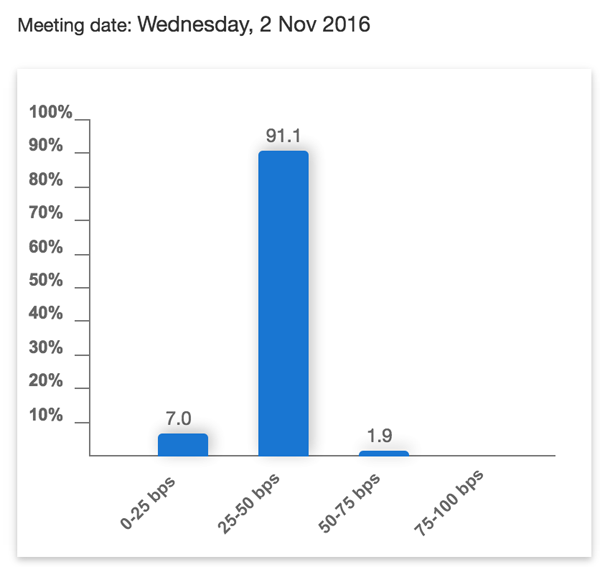

The “smart money” agrees: traders betting via the Fed funds futures market are now pricing in no rate hike until 2018. In fact, the odds of a rate cut are greater than those of a hike in the next six months. In case you missed it in last week’s article, here again is the current November spread:

The upshot? Strong dividend-growth stocks that had been weighed down by interest rate worries now have the green light. Here three that are great buys now.

The upshot? Strong dividend-growth stocks that had been weighed down by interest rate worries now have the green light. Here three that are great buys now.

Eaton Investors Voted “Leave”—Don’t Follow Them

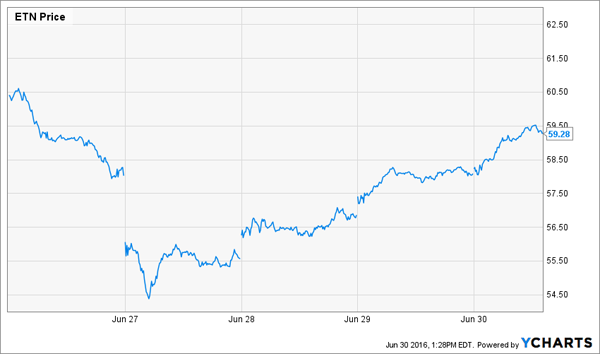

Eaton Corp. (ETN) was whacked after the Brexit vote, nosediving 13.5%, from $62.82 on June 23, when Britons were headed to the polls, to a low of $54.32. It’s now around $59.00.

As a result, Eaton trades at just 13.8 times forecast 2016 earnings—its lowest level in three months and a discount to competitors like Illinois Tool Works (ITW), at 18.4, and Cummins (CMI), at 14.1.

As a result, Eaton trades at just 13.8 times forecast 2016 earnings—its lowest level in three months and a discount to competitors like Illinois Tool Works (ITW), at 18.4, and Cummins (CMI), at 14.1.

First-level investors have avoided Eaton because the weak global economy is hitting demand for its hydraulic systems and industrial components. That’s likely to continue, with the company forecasting a 2% to 4% sales decline this year.

But dig deeper and you’ll see a firm with whip-smart management that’s deftly navigating the situation through targeted cost cuts and efficiency improvements.

Eaton forecasts earnings per share (EPS) of $4.15 to $4.45 this year—giving it a 50/50 shot at topping the $4.30 it posted last year. Analysts see EPS rising to $4.61 in 2017.

Either way, you’ll be well paid to stick around till things improve: ETN yields a tidy 3.9%, and payout hikes have come at a 19.2% annualized rate over the past decade. Even with those increases, the company only pays out 54% of its earnings as dividends.

JPM Won’t Be This Cheap for Long

There’s no doubt JPMorgan Chase & Co. (JPM) and the other big banks have had a rough six months. In December, they were giddy at the prospect of four interest rate hikes this year.

Fast-forward to today and they’re facing an even longer low-rate period, no thanks to Brexit. Meantime, oil producers, squeezed by the plunge in crude prices, are having a tough time repaying their loans. So it’s no surprise that Morgan’s stock has fallen 6.2% since the New Year.

But as the old saying goes, “The time to buy is when there’s blood in the streets.” Let’s tackle the overblown worries hovering over JPM, starting with energy exposure.

But as the old saying goes, “The time to buy is when there’s blood in the streets.” Let’s tackle the overblown worries hovering over JPM, starting with energy exposure.

It’s true that the bank has $44 billion of loans to oil and gas companies on its books. But exploration and development firms were hardest hit by crude’s freefall, and they only account for 2% of JPM’s total loans, or around $9 billion in all. Management has already set aside $1.3 billion to cover any defaults, which is plenty of slack, particularly with oil up 44% since February.

Meantime, JPMorgan is offsetting low interest rates by loaning out more cash. In the first quarter, strong loan volume, along with higher profits in consumer and community banking, kept its EPS above the Street’s expectations.

The shares yield 3.1% today, and with JPMorgan acing the Fed’s latest stress test last Wednesday, you can expect its strong payout growth—the quarterly dividend has nearly doubled in the past five years—to continue.

Adding more insurance is the bank’s bargain valuation, which limits its downside risk: JPMorgan trades right around book value (or what it would be worth if it were broken up and sold today) and only 10.9 times forecast 2016 earnings.

A “Boring” REIT With a Demographic Edge

Welltower Inc. (HCN) is the kind of stock you want to own when the markets throw a fit like they did after the Brexit vote.

With a beta rating of 0.43, Welltower is 67% less volatile than the market as a whole—and it showed last week, when the stock actually rose 0.5% in the two days following the vote, compared to a 5.3% plunge for the S&P 500.

The real estate investment trust owns 1,490 properties and is mainly focused on seniors’ housing. It’s not a flashy business to be in, but demographics are on Welltower’s side, with 10,000 baby boomers turning 65 every day (more on that below).

The growing senior population is translating into a steady increase in funds from operations (FFO)—a better measure of REIT performance than earnings—that Welltower is returning to investors in the form of a quarterly dividend that yields 4.5% annualized.

It’s a payout you can bank on: the dividend has risen at a 5.7% annualized rate since Welltower was founded in 1970, helping the REIT deliver a 15.6% average annual return in that time. In the past 12 months, FFO clocked in at $4.47 a share, easily covering the REIT’s $3.44 a share in dividend payments.

— Brett Owens

Double Welltower’s Yield With My Favorite Healthcare REIT [sponsor]

Welltower’s 4.4% yield is nice, but with the stock trading near a 52-week high, it’s understandable if buying now makes some investors nervous.

But what if I told you there’s a way to double that yield straight out of the gate, and at a bargain, to boot? I’m talking about a current payout of 8.7% from a REIT catering to the same booming senior-care market as Welltower.

This REIT specializes in skilled nursing facilities (SNFs), which provide the highest level of care a person can get while still living independently.

To say it’s off most investors’ radar is a huge understatement. It’s a recent spinoff, so just 3 lonely analysts cover it. But that’s changing, as a major investment bank recently initiated coverage.

I’m expecting big things from this one, with payout hikes that will have you yielding 10%+ on your initial investment in no time, plus annual price gains of 10%–15%.

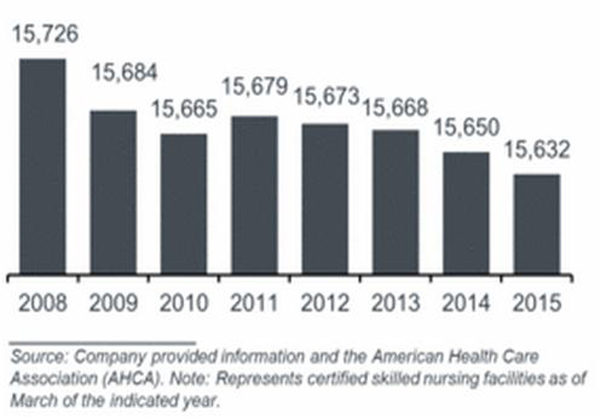

Because here’s the thing about the SNF market: even though demand is soaring, we actually have fewer SNFs than we did in 2009.

I know I don’t have to tell you that rising demand + falling supply = bigger profits. This firm is already capitalizing on this situation, and I expect it to announce its first big dividend by September.

I know I don’t have to tell you that rising demand + falling supply = bigger profits. This firm is already capitalizing on this situation, and I expect it to announce its first big dividend by September.

Don’t miss out. Click here to get [more information], and two more stocks that are cashing in on the biggest demographic shift in US history.

Source: Contrarian Outlook